How Retail Media Operated in 2025 | Topsort

Retail media crossed $163 billion globally this year. In the U.S., it's now nearly a quarter of all digital ad dollars—$60 billion and growing at 15-17% annually. The "third wave" narrative that dominated 2023 and 2024 is over. This is the baseline now.

But something shifted in 2025. The easy money from sponsored product listings started drying up. Amazon and Walmart locked down 84% of U.S. spend. Over 200 retail media networks launched or scaled, and brands found themselves managing campaigns across six to nine different dashboards—a number that looks set to hit eleven next year.

The conversation changed. It's no longer about whether to build a retail media network. It's about whether the one you're creating can actually compete. Before we get into what changed this year, here's how the technology actually works.

The three core functions

Strip away the marketing language, and retail media platforms do three things:

- They run auctions. When a shopper searches for "running shoes" on a retailer's site, the platform decides which sponsored products appear and in what order. This happens in milliseconds. The logic—who wins, at what price, based on what signals—is where platforms differentiate.

- They track attribution. Unlike traditional digital advertising, retail media has a clean feedback loop: did the person who saw the ad go on to buy the product? First-party purchase data makes this possible without the tracking gymnastics that plagued display advertising.

- They provide self-serve tools. Advertisers need to set budgets, choose targeting, upload creative, and monitor performance. The quality of this interface determines whether small and mid-sized brands can participate or whether the system is only available to those with agency support.

Simple enough in theory. The complexity is in execution.

How auctions actually work

Most retail media auctions use second-price models: the winner pays slightly more than the second-highest bid. This encourages honest bidding—you don't need to game the system because overbidding just costs you money without improving your chances.

But the real differentiator is what else goes into the ranking besides price.

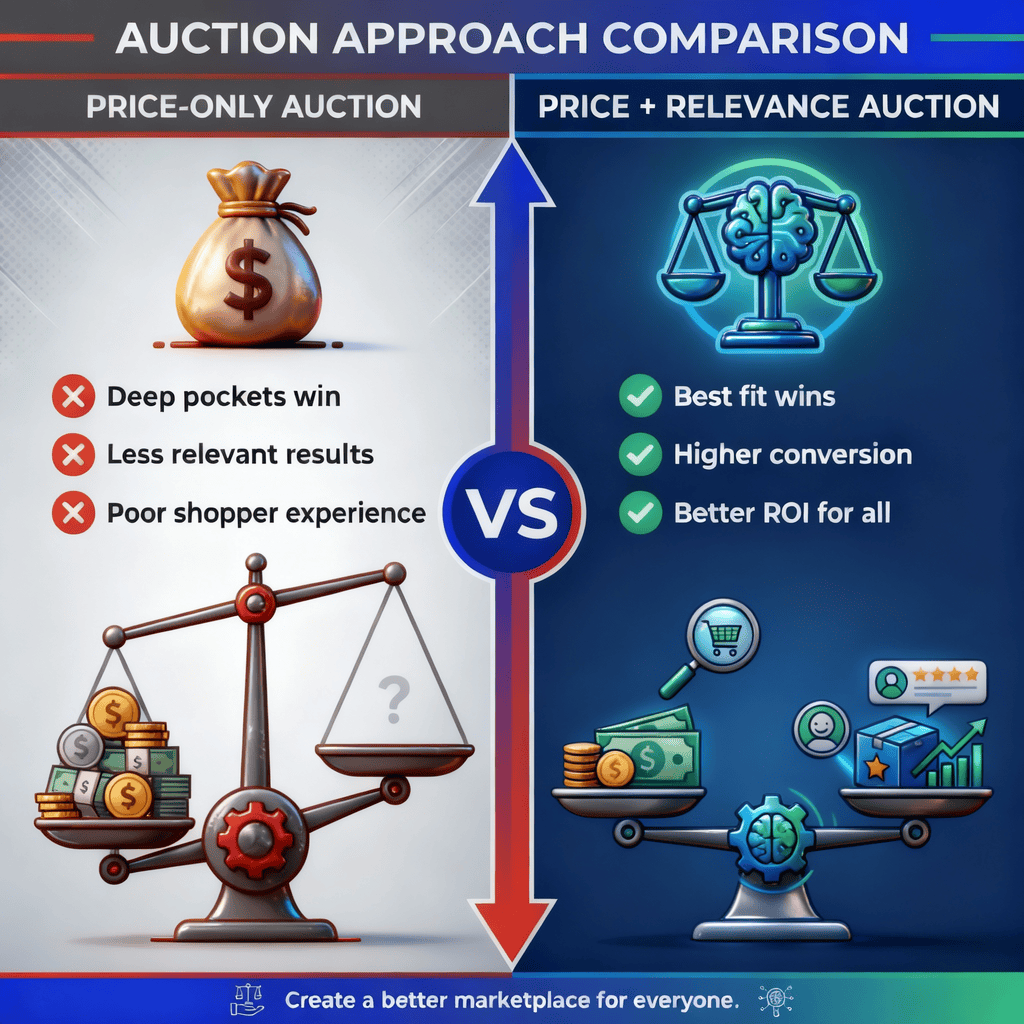

Pure price-based auctions create a problem: they reward deep pockets, not relevance. A well-funded brand can outbid everyone and show shoppers products they don't actually want. That's bad for the shopper, bad for the retailer's conversion rates, and ultimately bad for the advertiser's ROI.

The better approach blends bid price with predicted performance. If Product A is bidding $2 and has a 5% conversion rate, while Product B is bidding $1 and has a 12% conversion rate, a smart auction might favor Product B. The shopper sees something more relevant, the retailer makes more money over time, and the advertiser gets better returns.

This is where AI enters the picture—not as a buzzword, but as a practical necessity. Predicting which product will convert for which shopper in which context requires processing signals at a scale that rule-based systems can't handle. Platforms using automated allocation—where AI determines placement value based on predicted outcomes rather than on advertiser guesswork—are democratizing access and capturing long-tail revenue that competitors miss.

The privacy advantage

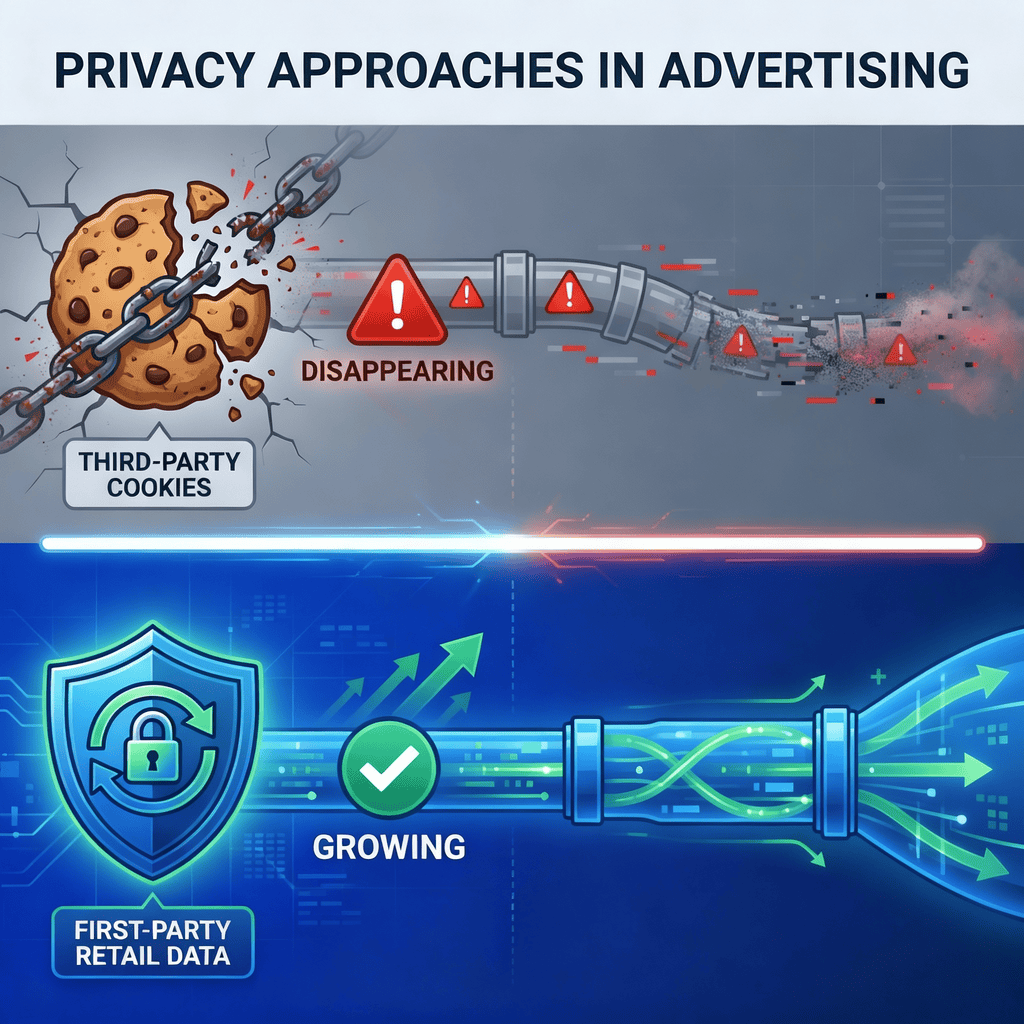

Retail media has a structural advantage: it doesn't need third-party cookies.

When someone browses a retailer's site, the retailer has first-party data—logged-in identity, purchase history, cart contents—collected in the context of a customer relationship. The targeting is contextual and transactional, not surveillance-based. Someone searching for "dog food" on a grocery site probably wants to see ads for dog food. Someone who bought diapers last month might be interested in baby wipes. No cross-site tracking required.

This isn't just a compliance advantage. It's a relevant advantage. Contextual signals—what someone is actively shopping for, right now—often outperform behavioral signals scraped from their browsing history.

That structural advantage became especially valuable in 2025.

What changed this year

Three problems surfaced in 2025 that most platforms haven't solved: fragmentation, incrementality, and speed to market. Here's what we learned.

The fragmentation tax became real

Every retailer built their own stack. Every stack had its own DSP, its own attribution window, its own definition of a conversion. By mid-2025, the industry had a name for what was happening: "advertiser fatigue."

This wasn't just a UX complaint. It was an economic problem. Brands started hiring entire teams just to manage logins and reconcile reporting across networks. The operational cost of managing 10 fragmented platforms began to eat into ROAS. Worse, it made unified frequency capping and cross-retailer attribution practically impossible, which meant wasted impressions and inflated costs.

The IAB released updated Commerce Media Measurement Standards in late 2024, but adoption this year has been uneven. The Tier 1 networks have the resources to implement them. The long tail often doesn't. The result is a two-speed market where advertiser dollars are starting to flow toward the platforms that offer standardized reporting and away from proprietary black boxes.

Are the retailers seeing 60% monthly ad revenue growth this year? They're the ones that went live in weeks, not quarters. Garmentory integrated retail media infrastructure in 48 hours. That became the new benchmark everyone else is now chasing.

For advertisers navigating this fragmentation, demand-side retail media platforms offer a way to unify access across multiple networks from a single interface.

Privacy regulations accelerated the shift

Google's cookie deprecation finally happened this year—sort of. Instead of a hard kill, Chrome started prompting users with a choice. The practical effect is the same: third-party cookies are disappearing through attrition. Eight new state privacy laws took effect in 2025. New Jersey now requires opt-in consent for anyone 13-17. Maryland has strict data minimization rules. The EU started enforcing the Digital Markets Act with actual penalties, forcing Amazon and others to crack open their walled gardens.

The surprise? This regulatory wave has been suitable for retail media. First-party data stopped being a buzzword this year and became a competitive moat. The platforms that can prove their targeting works better than cookie-based systems while being fully compliant out of the box are winning RFPs and brand evaluations.

The growth moved

Sponsored listings still account for 60-70% of network revenue, but growth there flattened to single digits this year. The high-intent pixels on search results pages are already monetized. The expansion in 2025 happened in three places:

Off-site programmatic grew 27-42%. Retailers started using their first-party data to buy ads across the open web, effectively turning themselves into data management platforms. U.S. advertisers spent over $20 billion on this in 2025 alone.

Video and CTV jumped 43%. Retailers partnered with streaming platforms—Amazon Prime Video, Walmart's Vizio acquisition, Kroger's Roku integration—to capture brand-building budgets that used to go to linear TV. Video ads captured 86% of new display ad spending this year.

In-store digital grew 47%. With 70-85% of retail transactions still happening in physical stores, the screens on shelves, at checkout, and at the entrance represented the most extensive untapped inventory. The technical challenges are real—foot traffic measurement, inventory sync, and latency—but the retailers solving them are building compounding data assets.

The definition of "retail media" also expanded to include "commerce media" this year. Chase and PayPal built financial media networks using transaction data. United Airlines and Marriott started monetizing traveler audiences. The platform providers that can support these adjacent verticals are capturing share outside traditional retail.

The incrementality question got serious

The uncomfortable question finally came to the fore this year: Are the ads driving purchases that wouldn't have happened otherwise, or are they just taxing transactions that would have occurred anyway?

Most platforms can report ROAS. Far fewer can prove incrementality. Only 25% of organizations say they're proficient at measuring it. The issue is structural—walled gardens make it hard to run proper holdout tests, and attribution models tend to over-claim credit for sales that would have happened organically.

Advertisers stopped accepting "attributed sales" as a proxy for performance in 2025. They started demanding lift studies, holdout testing, and transparent SKU-level reporting. The platforms that couldn't deliver started losing budget to those that could.

The shift is just beginning, but it's clear where this goes. Incrementality is becoming the primary KPI. That means building measurement infrastructure that supports true experimentation—clean control groups, third-party verification, auditable data. It also means educating advertisers on what "good incrementality" looks like, because most are still learning.

Automated bidding stopped being optional

Manual bidding remained a barrier to entry all year. Small advertisers—the long tail that represents the most significant revenue opportunity—don't have the time or expertise to optimize bids across campaigns. Traditional ad platforms place the burden on the advertiser to determine what to bid. That works fine if you're Procter & Gamble with a dedicated media team. It doesn't work if you're a small vendor with a $500 monthly budget.

Poshmark implemented automated bidding this year and saw a 43% increase in sales and a 3.8x ROAS, driven partly by making the system accessible to over 1,000 sellers who couldn't have managed traditional campaigns. That result got attention. Autobidding is shifting from a premium feature to a table-stakes feature. The platforms that democratize access—making it genuinely easy for small advertisers to participate and win—are capturing long-tail revenue that competitors can't reach.

What happens next

The numbers tell the story. Global retail media spend is projected to hit $200 billion in 2026, $220 billion in 2027, and potentially $300 billion by 2030—larger than the entire global television advertising market. By 2028, retail media will account for a full quarter of all digital ad spend.

The consolidation has already started. Smaller retailers are abandoning standalone ad tech stacks in favor of infrastructure providers because the cost of going it alone doesn't pencil out. The Tier 1 giants—Amazon, Walmart, and Instacart—will continue to build proprietary systems. Everyone else needs partners.

Three things are about to define the market:

Standardization becomes a competitive weapon. Advertisers will shift budgets toward platforms that offer consistent measurement and interoperability. Fragmentation becomes a liability.

Incrementality replaces ROAS as the KPI. The platforms that can prove lift—not just report attributed sales—will capture the largest share of new budgets.

Automation unlocks the long tail. The networks that make it genuinely easy for small advertisers to participate will capture revenue that others can't access.

At Topsort, retail media isn't about whether to build a network anymore. It's about creating one that can compete in a maturing, consolidating market where the standards are rising fast. Whether you're a retailer building your own network or an advertiser looking to buy across multiple networks, we've built solutions for both sides—including Toppie for demand-side buying.

The technology that wins will be the technology that makes complexity manageable: auctions that optimize automatically, integrations that take days instead of months, tools that small advertisers can use without training, and measurement that everyone trusts.

The infrastructure decisions happening right now—in the last weeks of 2025—are determining who captures the $40 billion in incremental spend projected to flow into the category next year.